-3.0 percent decrease in the national average of warehouse storage costs year-over-year in Q4 ’24 vs Q4’ 23, with a -0.6 percent decrease over the last quarter

The national average of warehouse storage costs has seen a decrease in 12 consecutive months

The overall industrial vacancy rate rises 20 basis points to 6.7%, signaling the market may reach peak vacancy soon

The Warehouse Pricing Index (WPI) is available in the Journal of Commerce’s extensive, multi-channel dashboard, Gateway. Learn more about Gateway and how WarehouseQuote is helping logistics managers make smart supply chain decisions.

U.S. Warehousing Market Watch

6.7% National Industrial Vacancy Rate

-3.0% YOY Decrease in the National Average of Warehouse Storage Costs

Retailers Brace for Potential Tariffs on U.S. Imports

Retailers are proactively adjusting their supply chains in anticipation of potential tariffs on imports, particularly from China, Mexico, and Canada, as proposed by President Donald Trump. These measures include diversifying manufacturing locations, renegotiating supplier agreements, and considering price adjustments to mitigate the impact of increased duties.

Companies like Yeti and Traeger are expanding production outside of China to reduce tariff exposure. Yeti aims to have 50% of its drinkware capacity outside China by the end of 2025, while Traeger is increasing manufacturing in Vietnam.

Retailers are also contemplating price adjustments to offset additional costs. Traeger, for instance, has indicated that pricing is a lever they might use to mitigate the downside of tariffs. Additionally, companies like TJX are looking to capitalize on inventory surpluses created by vendors bringing in goods early to minimize risk, potentially allowing them to acquire products at favorable prices.

At a national level, WarehouseQuote expects to see a subtle increase in warehouse services pricing, driven by tightening industrial real estate vacancy rates and companies front-loading inventories into the U.S. amid tariffs on imports. Advanced stocking of commodities manufactured overseas that have historically avoided trade tariffs, could further fuel costs of warehousing activity in the United States.

At a regional level, however, we are still seeing ample warehouse space in tier 2 and 3 markets. We see this as a great market opportunity for companies looking to adopt a forward-stocking inventory strategy outside of tier 1 markets, where activity is increasing.

Additionally, logistics and supply chain managers found procuring warehouse space on the West Coast to be much easier in 2024 versus previous years. This year, we expect it to become more challenging. Shippers seeking warehouse space in 2025 can tap into WarehouseQuote’s flexible network of 1000’s of vetted providers.

National Warehouse Pricing Index

The National Warehouse Pricing Index (WPI) decreased in Q4 '24 vs Q4’ 23,down 3.0 percent year-over-year. The ample amount of available space in the market is shown with the marginal drop in the national warehouse rate index.

Regional Warehouse Pricing Index

All U.S. regions have seen a pricing decrease year-over-year for warehousing services. The Midwest was marginally down at -0.4%, followed by steeper declines in the Northeast, South, West regions at -3.2%, -3.0%, and -4.2%, respectively.

The Voice of WarehouseQuote

“While the industrial vacancy rate continues to rise, the rate of the climb is decelerating. Coupled with a renewed sense of urgency for front-loading inventory into the US, we expect a reversal of the wait-and-see approach that so many supply chain service providers experienced through 2024.” - Jordan Brunk, Chief Marketing Officer at WarehouseQuote

Exclusive Commentary from S&P Global Market Intelligence and C.H. Robinson

To front load, or not to front load: Supply chain strategies in the face of tariffs

Chris Rogers Head of Supply Chain Research, S&P Global Market Intelligence

There should be no surprise that US trade policy will be the defining factor for supply chain decision-makers in 2025. President Trump is committed to wide-ranging import duties, but the big questions are who they will be applied to, how high will they be set and which countries will be exempt.

One option is that tariffs cover most countries, but the Trump administration may pursue an escalating scale of import duty increases, rather than applying the full force of tariffs immediately. That could see duties on imports from a wide range of trade partners increase by up to 5% points per month using the International Emergency Economic Powers Act.

All tariff outcomes remain possible at this stage, though the most likely outcome includes a widening and raising of tariffs on imports from mainland China and the imposition of duties on most other trade partners – possibly even including those with a free trade agreement.

The uncertainty leaves US importers, particularly of consumer goods which are either seasonal or perishable, having to decide whether to continue to “front-load” their imports after the US east coast port strike was averted.

The evidence for front-loading is clear from trade data of a variety of sources. Total exports of all products from mainland China to the US climbed by 15.6% year over year in December, according to official data, the fastest rate of growth for a single month since the pandemic-era rebound in June 2022. Similarly, US seaborne imports of consumer discretionary goods from mainland China increased by 15.8% year over year in December, led by a 24.2% jump in consumer electronics and a 23.6% rise in apparel.

However, US retail inventory-to-sales ratios – a measure of retailers’ stance on supply volatility – experienced only a small uptick in November to 1.14x from 1.13x a month earlier excluding autos, according to official data. That’s the same level as most of 2024 after a decline from peak of 1.20 in March 2023 to 1.13 in 2024.

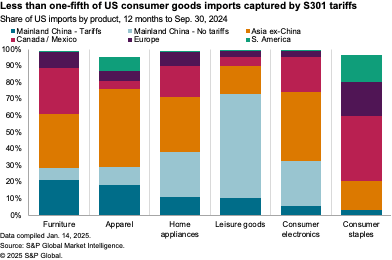

Looking across consumer goods, only 32.7% of US imports of consumer discretionary and staples products from mainland China are covered by Section 301 duties so far. That equates to 8.9% of all US imports of those products, Market Intelligence data shows. If all imports from mainland China became subject to duties, the share of US imports of consumer goods covered by tariffs on imports from China would rise to 27.2%.

The increase would be particularly notable for leisure goods (toys and exercise equipment) where coverage would increase to 73.2% of US imports from 10.4% currently, home appliances (38.1% from 11.0%) and consumer electronics (32.7% from 5.9%).

Looking into the rest of the year US import volumes in the first quarter of 2025 could still be solid. Market Intelligence forecasts call for total trade to rise by 8.8% year over year in nominal dollars in the first quarter of 2025, led by consumer goods (e.g. furniture is forecast to increase by 13.4%) and electronics (8.3%).

Containerized freight is expected to follow a similar track to total trade, with growth forecast at 11.5% year over year in the first quarter. The impact of tariffs will be felt in lower imports through the whole year, however, with total TEUs imported forecast to fall by 4.4% year over year in 2025 as a whole.

The sectors with the fastest downturns are those exposed to blanket tariffs on imports from mainland China, which will be applied at a higher rate than other countries, for example imports of toys are expected to fall by 12.6% year over year, while apparel is forecast to fall by 9.5% and electronics by 9.1%.

Navigating the Ripple Effects of a Port Strike Avoided: Insights and Market Trends

Mathew Leo Principal Manager, Research and Market Intelligence, C.H. Robinson

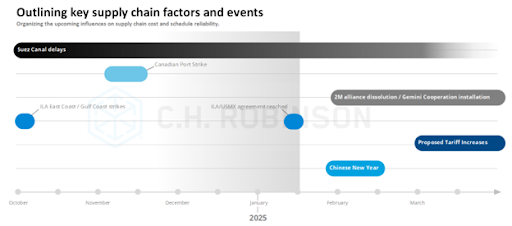

As 2025 unfolds, the freight and transportation industry continues to face significant changes, balancing resilience with evolving market dynamics. While the recent avoidance of a port strike is a relief for shippers and the broader economy, its ripple effects are already reshaping supply chains and transportation modes. In addition to this, winter storms, wildfires, proposed tariff increases, ocean carrier alliance shifts, and other various events create further complexity. Here's a closer look at what’s next.

Potential Tariff Pull-Forward

The very thought of tariffs has shaken up supply chains. While speculation exists on how countries like China, Canada, and Mexico will be impacted, some shippers have taken action. Since changing suppliers is not typically an overnight task, these shippers have pulled forward some of those orders to get ahead of the tariffs. This means more inventory on hand and an increase in demand for warehousing on the west coast. Potential tariffs on specific commodities, such as solar energy components or lithium-ion EV batteries, could create an outsized impact on certain industries. Closely monitoring not just the countries but the commodities impacted will be critical.

The Aftermath of the Avoided Port Strike

The resolution of the East/Gulf Coast port labor issue has brought relief but not without lingering complexities. Many shippers had preemptively shifted freight to West Coast ports, a trend expected to partially reverse. However, a mass exodus back to East/Gulf ports is unlikely.

Factors like the ocean freight market’s current alignment with West Coast routes, the complexity of reverting supply chains, and the specter of potential tariffs are incentivizing many shippers to maintain the status quo until greater clarity emerges.

Modal Impacts: A Closer Look

Ocean Freight: While the avoided strike sets the stage for potential rate softening, active disruptions like the Ocean Alliance reshuffling, Chinese New Year, and Suez Canal diversions will keep rates under pressure.

Air Freight: The strike resolution has negligible impact on air freight. The other disruptions and modal capacity will have a greater impact.

Truckload (TL): TL rates are unlikely to decrease due to this event, though the resolution may curb potential rate hikes. Regional pricing shifts are anticipated as supply chains adjust.

Less-than-Truckload (LTL): Minimal impact on LTL rates is expected.

Intermodal (IMDL): As supply chains shift eastward, IMDL volumes may decline since the East Coast’s proximity to population centers reduces the need for long-haul rail transport.

Economic and Operational Implications

The resolution is undoubtedly positive for the economy and shippers alike. It does underscore the importance of a global, multimodal solutions approach that C.H. Robinson offers. The ability to plan for contingencies, offer alternative modes, and leverage diverse port options has proven invaluable during this disruption.

For time-sensitive commodities like produce from countries such as Peru, the resolution alleviates the risk of spoilage and costly rerouting. These shippers can now focus on timely deliveries without the shadow of alternative arrangements hanging over their operations.

Market Updates and Forecasts

Current Market Equilibrium: The freight market has reached a state of relative balance, meaning disruptions like this are felt more acutely compared to the past two years. While temporary effects dominate for now, their lasting impact remains uncertain due to the high volume of carrier supply.

Truckload Forecast:

Shippers pulling forward shipments to mitigate potential future strikes or tariffs have created short-term regional volume shifts, driving minor spot pricing adjustments.

Despite these fluctuations, the truckload market remains oversupplied, limiting significant near-term spot rate changes.

In 2024, dry van linehaul costs per mile ended 4% below 2023 levels. Projections for 2025 anticipate a 9% year-over-year increase, influenced by market recovery and continued labor and weather-related risks.

Natural Disasters and Seasonal Effects:

The first week of 2025 brought fires in Los Angeles and widespread snowstorms, disrupting both supply and demand.

On the supply side, road closures and safety concerns have slowed operations. For demand, priorities have shifted in affected areas, reducing immediate freight requirements.

These dynamics may balance each other, but full data will shed light on their net effect.

Economic Considerations Beyond Freight

Broader economic implications are also emerging, particularly in California. Rebuilding efforts from fires and other disasters will spur economic activity. However, rising insurance premiums and housing costs could dampen consumer confidence, potentially affecting long-term spending patterns.

Looking Ahead

The resolution of the East/Gulf Coast labor situation is a reminder of the interconnected nature of global supply chains and transportation networks. While immediate impacts are beginning to unfold, the longer-term implications—shaped by shifts in demand, economic conditions, and regulatory developments—will require close monitoring.

For shippers and industry stakeholders, adaptability remains key. Strategic planning, multimodal capabilities, and scenario-based forecasting will be crucial tools to navigate these evolving landscapes effectively.

In partnership with the U.S. Chamber of Commerce, RSM has collected data on middle market firms since 2015 through quarterly surveys conducted by The Harris Poll. The RSM US Middle Market Business Index provides a leading measure on the performance of businesses that make up the heart and soul of our country's economy.

Logistics Managers Index

The LMI score is a combination of eight unique components that make up the logistics industry, including: inventory levels and costs, warehousing capacity, utilization, and prices, and transportation capacity, utilization, and prices. The LMI is calculated using a diffusion index, in which any reading above 50.0 indicates that logistics is expanding; a reading below 50.0 is indicative of a shrinking logistics industry.

Industrial Real Estate Vacancy Rates

Industrial real estate vacancy rate is the percentage of available industrial property, such as a warehouse or distribution center.

United States Regional Divisions

Midwest

East North Central: Illinois, Indiana, Michigan, Ohio, and Wisconsin

West North Central: Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, and South Dakota

Northeast

New England: Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, and Vermont

Middle Atlantic: New Jersey, New York, Pennsylvania

South

South Atlantic: Delaware, Florida, Georgia, Maryland, North Carolina, South Carolina, Virginia, Washington DC, and West Virginia

East South Central: Alabama, Kentucky, Mississippi, and Tennessee

West South Central: Arkansas, Louisiana, Oklahoma, and Texas

WarehouseQuote’s Economic Commentary Disclaimer

The material and content used in this publication is for informational purposes only. Reference to any third party (including external hyperlinks) does not constitute or imply the endorsement of said third party. WarehouseQuote does not warrant the accuracy or completeness of the Content. The views and opinions expressed herein are those of the author and do not necessarily reflect the official policy or position of WarehouseQuote. Reproduction of the Content may be made only with the written permission from WarehouseQuote.

WarehouseQuote is a managed warehousing solution helping middle market and enterprise businesses scale their warehouse operations with precision. Through our 3PL warehousing and fulfillment network of 250+ facilities, integrated technology platform, and in-house supply chain expertise, we enable businesses to design efficient fulfillment networks connected by a single technology platform. Hundreds of B2B and B2C businesses like Chatime, Joyride, Benitago Group, Big Ass Fans, and Mighty Good Solutions use WarehouseQuote to scale, streamline, and optimize their warehouse operations.